What is the Forklift Battery Market Overview – definition, scope, and significance?

The Forklift Battery Market comprises manufacturers, distributors, and service providers of power sources used in material handling equipment, primarily forklifts. Batteries are classified by type (Lithium‑Ion, Lead‑Acid), capacity (0‑600 Ahr, 600‑1200 Ahr, >1200 Ahr) and application (manufacturing, construction, warehouse & logistics, automotive, retail & wholesale). The market’s significance stems from its role in enabling efficient material movement, reducing operational costs, and supporting automation trends in logistics and production facilities. As warehouses expand and e‑commerce accelerates, reliable power solutions become critical, driving demand for advanced battery technologies.

What are the Forklift Battery Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include the shift toward electric forklifts for sustainability, the superior cycle life of Lithium‑Ion batteries, and rising automation in warehouses. Restraints involve the higher upfront cost of Lithium‑Ion solutions and the limited recycling infrastructure for Lead‑Acid batteries. Challenges comprise regulatory compliance for safety and emissions, and the need for robust charging infrastructure in legacy facilities. Opportunities arise from the growing need for fast‑charging, high‑energy‑density batteries, and from emerging markets investing in modern material‑handling fleets.

What are the current Forklift Battery Market Growth Trends?

Trend analysis shows a clear transition from Lead‑Acid to Lithium‑Ion batteries, driven by longer lifespan and lower total cost of ownership. Manufacturers are introducing modular battery packs that support quick swap‑out, reducing forklift downtime. Additionally, smart‑battery management systems are being integrated to monitor health, temperature, and charge cycles, enabling predictive maintenance. The market also sees increased adoption of high‑capacity (>1200 Ahr) batteries for heavy‑duty applications.

How did COVID‑19 impact the Forklift Battery Market and what is the recovery trajectory?

The pandemic temporarily disrupted supply chains, causing delays in component deliveries and slowing new equipment purchases. However, the surge in e‑commerce and the need for socially distant, automated warehousing accelerated demand for electric forklifts and their batteries. Post‑2020, the market rebounded swiftly, with growth momentum maintained by the shift to contact‑less operations. The recovery is now consolidated, supported by stronger inventory levels and renewed capital spending in logistics hubs.

Who are the major competitors in the Forklift Battery Market and what is the competitive landscape?

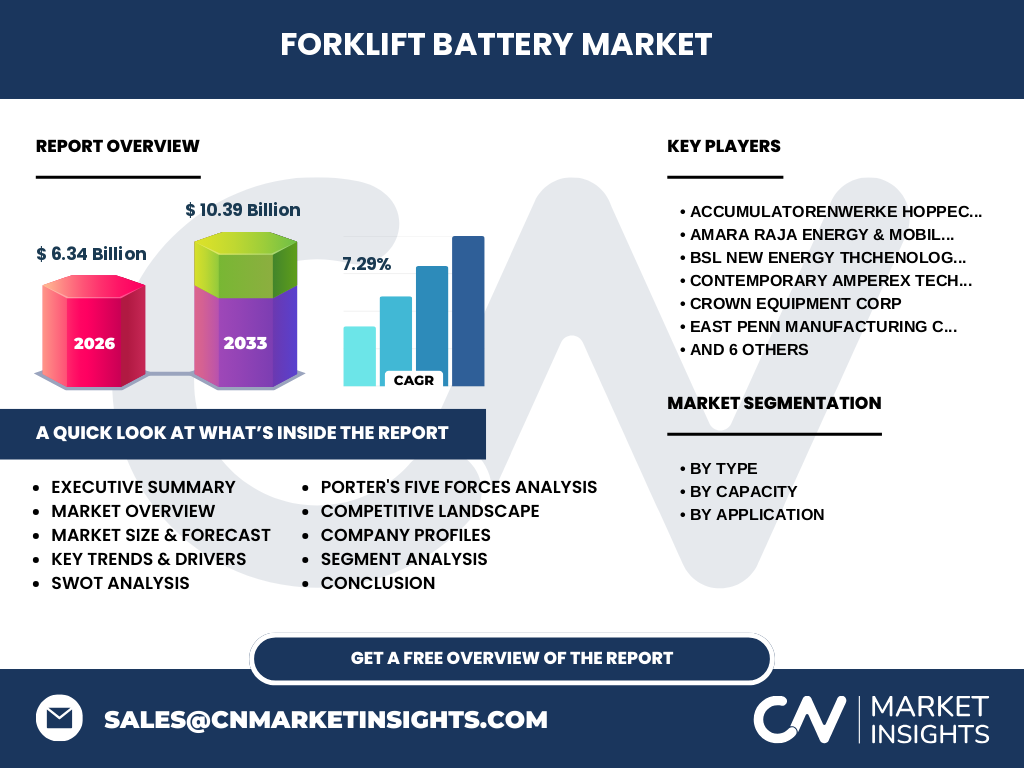

The market is moderately consolidated with a mix of global battery manufacturers and specialist forklift power‑train providers. Leading players include Accumulatorenwerke HOPPECKE, Amara Raja Energy, BSL New Energy Technology, Contemporary Amperex Technology (CATL), Crown Equipment Corp, East Penn Manufacturing, EnerSys, Exide Industries, GS Yuasa, TAB d.d., TotalEnergies, and Leoch International. Companies compete on technology (Lithium‑Ion vs. Lead‑Acid), capacity range, service networks, and strategic partnerships with forklift OEMs. Mergers and joint ventures are common as firms seek to broaden product portfolios and geographic reach.

What is the Executive Summary – high‑level overview and key findings?

The Forklift Battery Market is valued at USD 6.34 billion in 2026 and is projected to reach USD 10.39 billion by 2033, reflecting a CAGR of 7.29 %. Lithium‑Ion technology is gaining market share due to its operational efficiency, while Lead‑Acid remains important in cost‑sensitive segments. Capacity demand is skewing toward >1200 Ahr units for heavy‑duty use. Regional demand is strong in industrialized economies, with growth pockets in emerging logistics hubs. Competitive dynamics are shaped by technology innovation, service integration, and strategic alliances.

What are the Forklift Battery Market Forecasts for 2025‑2032?

Based on the provided CAGR of 7.29 %, the market will continue expanding steadily. By 2027 the market is expected to surpass the USD 7 billion threshold, and by 2032 it will approach the upper end of the forecast range, nearing USD 10 billion. Growth will be propelled by the replacement cycle of aging Lead‑Acid fleets, increased adoption of Lithium‑Ion batteries in new forklift purchases, and expanding capacity requirements in high‑throughput warehouses.

How is the Forklift Battery Market sized and shared by segmentation?

By type, the market splits between Lithium‑Ion and Lead‑Acid, with Lithium‑Ion capturing the faster‑growing segment due to higher performance and lower lifecycle cost. By capacity, the three bands—0‑600 Ahr, 600‑1200 Ahr, and >1200 Ahr—reflect application needs, where the >1200 Ahr segment is seeing the strongest growth driven by heavy‑duty forklifts. By application, the warehouse & logistics segment dominates, followed by manufacturing, construction, automotive, and retail & wholesale stores, each contributing to overall demand based on their material‑handling intensity.

What is the Global Forklift Battery Market size and share by region?

The global market totals USD 6.34 billion in 2026. While precise regional breakdowns are not disclosed, the market is driven by North America and Europe’s mature logistics infrastructure, Asia‑Pacific’s rapid industrial expansion, and growing demand in Latin America and the Middle East for modern material‑handling solutions. These regions collectively account for the full market value.

What does the Regional Analysis of the Forklift Battery Market reveal?

North America benefits from high automation rates and stringent emissions standards, encouraging forklift electrification. Europe’s focus on green logistics supports Lithium‑Ion adoption. Asia‑Pacific, led by China and India, shows the highest volume growth due to expanding manufacturing bases and warehouse construction. Emerging economies in Africa and the Middle East are gradually increasing procurement of electric forklifts as infrastructure improves.

What are the leading company profiles and their strategies?

Accumulatorenwerke HOPPECKE emphasizes premium Lead‑Acid solutions with extensive service networks. Amara Raja Energy focuses on cost‑effective Lithium‑Ion packs for Asian markets. BSL New Energy invests in high‑capacity modules for heavy‑duty use. CATL leverages its global battery R&D to supply advanced Lithium‑Ion systems. Crown Equipment integrates batteries with its forklift designs, offering turnkey solutions. EnerSys and Exide Industries provide diversified power products across multiple industries, while GS Yuasa and Leoch International target niche high‑performance applications. TotalEnergies utilizes its energy portfolio to develop sustainable battery chemistry.

How does Porter’s Five Forces analysis apply to the Forklift Battery Market?

Threat of new entrants is moderate; high capital requirements and technology expertise deter many newcomers. Bargaining power of suppliers is moderate, as raw materials like lithium are concentrated but alternative chemistries exist. Bargaining power of buyers is strong; large warehouse operators negotiate volume discounts and demand service guarantees. Threat of substitutes is low; alternative power sources (hydrogen fuel cells) are still nascent for forklifts. Industry rivalry is intense, with firms differentiating on technology, capacity offerings, and after‑sales support.

What are the SWOT insights for the Forklift Battery Market?

Strengths: Essential role in material handling, growing shift to electric power, clear cost‑benefit over lifecycle.

Weaknesses: High upfront cost for advanced batteries, limited recycling infrastructure for certain chemistries.

Opportunities: Development of fast‑charging, modular battery systems, expansion in emerging logistics hubs, integration with IoT for predictive maintenance.

Threats: Raw material price volatility, regulatory changes affecting battery disposal, competition from alternative propulsion technologies.

What does the Forklift Battery Market value chain look like?

The value chain starts with raw material extraction (lithium, lead, electrolytes), followed by cell manufacturing, module assembly, and system integration with forklift OEMs. Distribution channels include direct sales to large logistics firms and indirect sales through distributors. After‑sales services—installation, charging infrastructure, maintenance, and end‑of‑life recycling—complete the chain, creating additional revenue streams for manufacturers.

What key investment insights can be drawn from the Forklift Battery Market?

Investors should prioritize companies with strong Lithium‑Ion R&D pipelines and those establishing charging ecosystem partnerships. Firms that offer integrated battery‑as‑a‑service models can capture recurring revenue. Geographic diversification into Asia‑Pacific logistics expansions provides growth leverage. Monitoring regulatory trends on emissions and battery recycling will help anticipate market shifts.

What is the conclusion of the Forklift Battery Market analysis?

The Forklift Battery Market is on a robust growth trajectory, underpinned by sustainability goals, automation, and the superior economics of modern battery technologies. While challenges remain—particularly cost and recycling—ongoing innovation and strategic partnerships are expected to sustain a CAGR above 7 % through 2033. Stakeholders who align with the emerging Lithium‑Ion focus and invest in service‑oriented business models will be best positioned to capture value.

How was the research methodology designed for this report?

The study combined primary interviews with industry executives, secondary data from company filings, trade publications, and market databases. Quantitative analysis applied the provided CAGR to project future market size, while qualitative insights were derived from expert opinions on technology trends, regulatory impacts, and competitive dynamics.

What is the scope of this research?

The scope covers global Forklift Battery market sizing, segmentation by type, capacity, and application, regional performance, competitive landscape, and forward‑looking forecasts to 2033. It excludes detailed financial breakdowns beyond the supplied market values and does not quantify individual company market shares.

Who are the key companies and what recent developments have they announced?

Key players include Accumulatorenwerke HOPPECKE, Amara Raja Energy, BSL New Energy, CATL, Crown Equipment, East Penn Manufacturing, EnerSys, Exide Industries, GS Yuasa, TAB d.d., TotalEnergies, and Leoch International. Recent developments feature CATL’s launch of a high‑energy‑density Lithium‑Ion pack for >1200 Ahr forklifts, Crown Equipment’s rollout of a battery‑swap service in North America, TotalEnergies’ partnership to develop recyclable battery chemistry, and Leoch International’s expansion of a fast‑charging network in Southeast Asia.